Stochastic Modeling for Energy Contract Terms Selection

Engagement Overview

A leading construction materials firm sought to reduce its long-term electricity costs by contracting wind-generated power from a company-owned renewable energy project. The engagement involved a rigorous financial evaluation of two competing long-term Power Purchasing Agreement (PPA) offers — analyzing net present value (NPV), risk exposure, and strategic fit across multiple scenarios to inform executive-level decision-making.

The Challenge

The client owned a wind energy generation project and faced a pivotal decision: sell the project outright under a long-term PPA with one of two competing energy suppliers, or retain it without a supply agreement with the parent company. Two credible offers were on the table — one from a project-finance-backed independent power producer (Supplier A) and one from a self-funded global energy utility (Supplier B) — each with materially different commercial structures, risk profiles, contract durations, and volume commitments.

Supplier A offered a 20-year variable-volume contract (750–1,100 GWh/year) with as-produced delivery and an early transition from a legacy power agreement, while Supplier B proposed a 15-year fixed-volume guaranteed delivery contract (700 GWh/year) with a known daily delivery profile. The core analytical challenge was to determine which offer maximized value across a range of future market scenarios — from a base case through to stressed conditions — while accounting for structural differences in volume flexibility, delivery certainty, contract duration, and sensitivity to electricity market price deterioration.

Approach & Methodology

The analytical framework was built around three scenario tiers — Base, Risk, and Stress — to capture the full range of plausible market outcomes over a 22-year analysis horizon. The Base scenario relied on third-party electricity market price projections, while the Risk scenario incorporated accelerated renewable energy penetration, structural renewable energy certificate (REC) oversupply, and the influence of cheap natural gas on marginal pricing. The Stress scenario was reverse-engineered to identify the market price trajectory at which each contract would generate zero net present value (NPV).

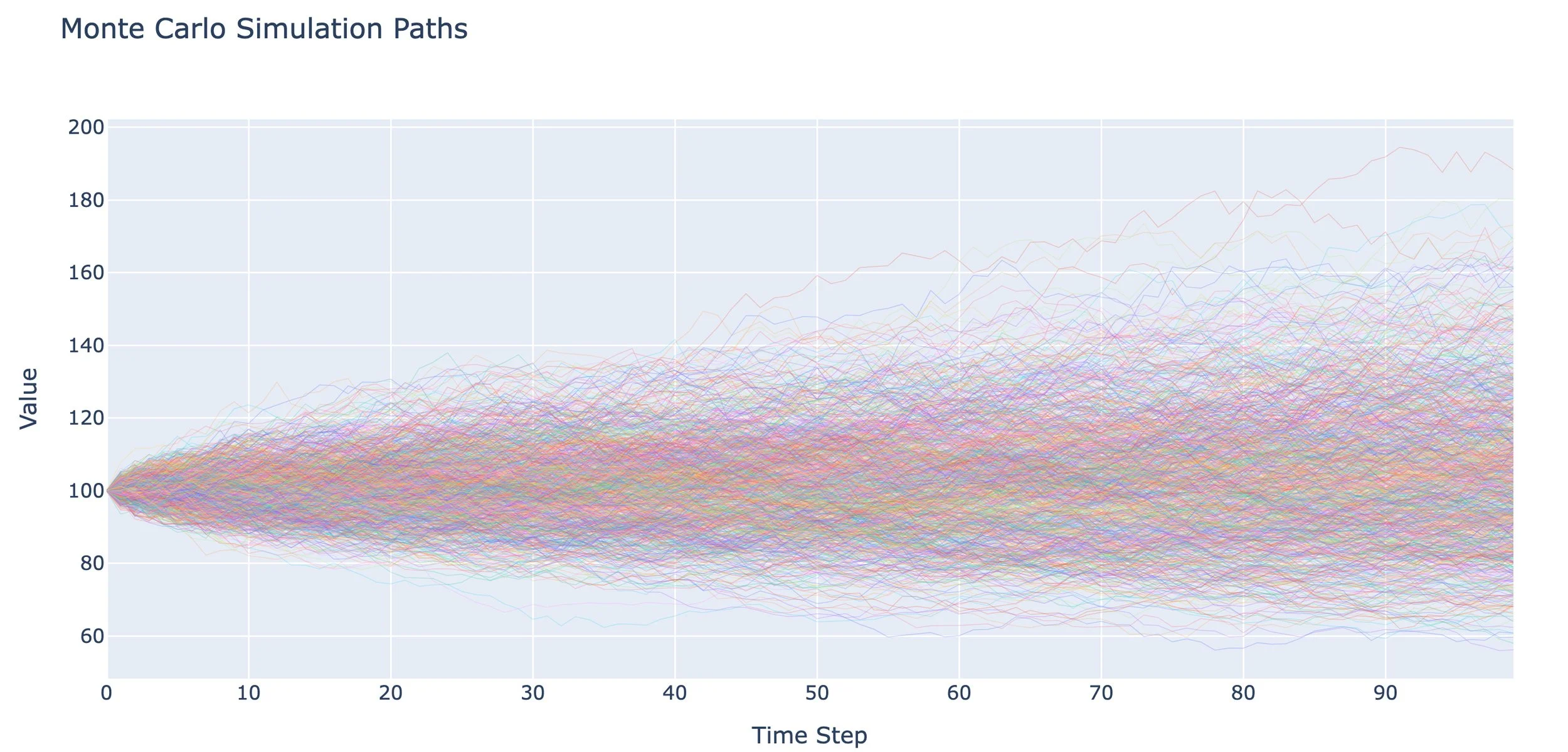

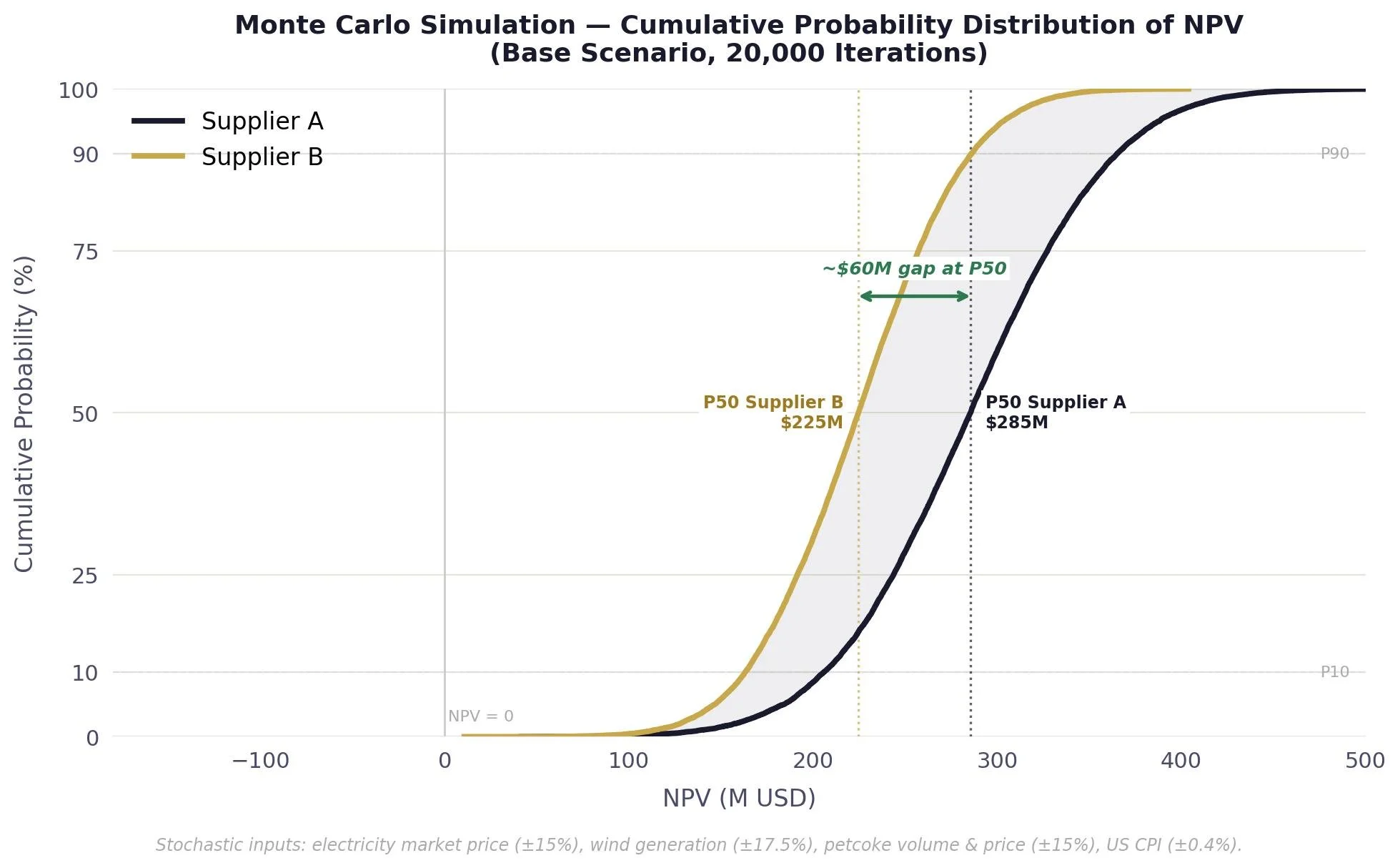

A stochastic financial model was developed to quantify NPV sensitivity across the key value drivers: electricity market prices, wind park generation output, REC prices, fuel costs from a state-owned supplier, and U.S. inflation. Monte Carlo simulation generated cumulative probability distributions of NPV savings under each offer, enabling a probabilistic comparison rather than reliance on point estimates alone.

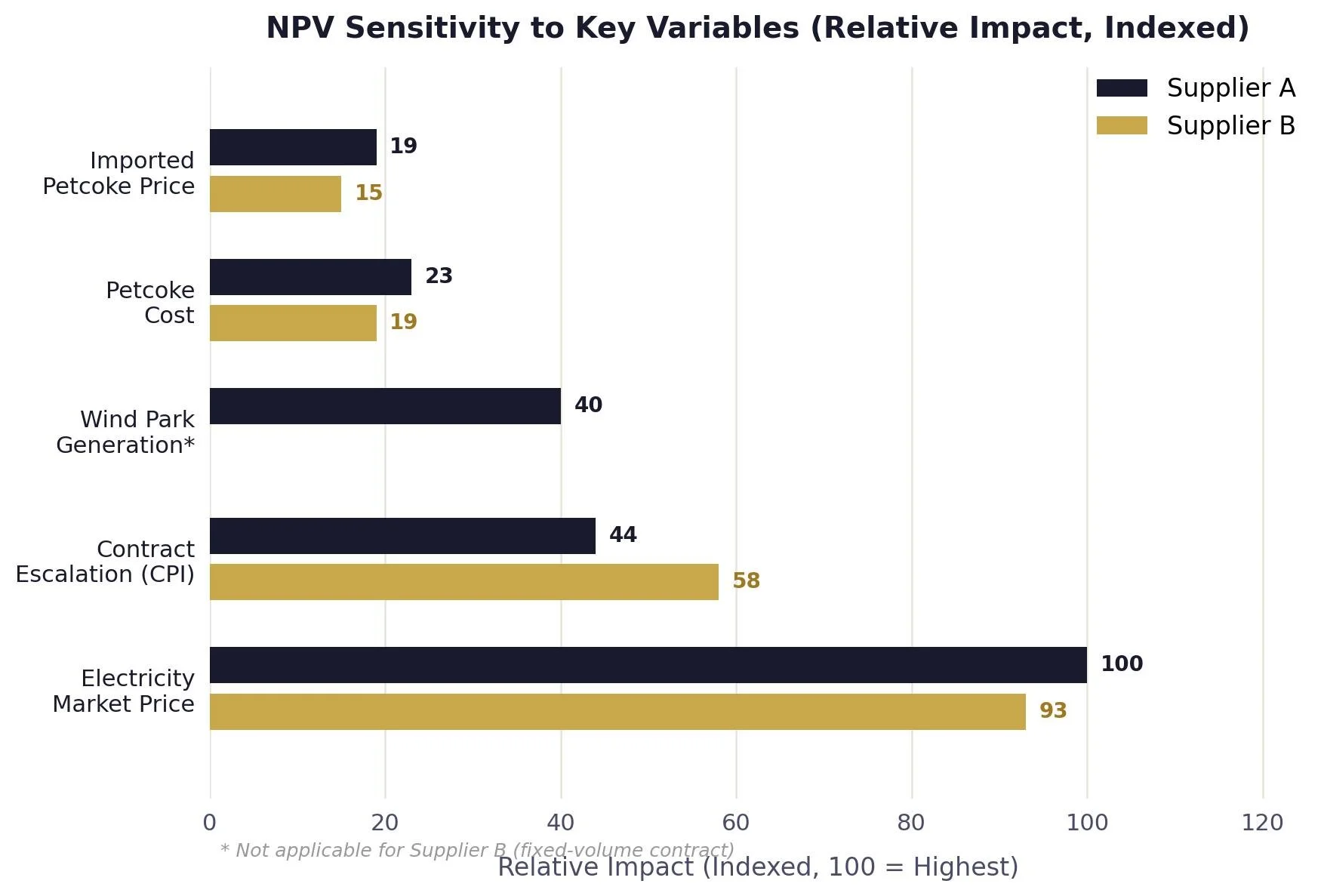

Annual cash flow modelling dis-aggregated value by source — electricity energy savings, REC surpluses and deficits, capacity payments, legacy agreement migration benefits, and asset sale proceeds — providing visibility into both total NPV and the timing and composition of value creation. Sensitivity and tornado analyses identified energy market price as the dominant driver under both contracts.

Key Deliverables

Three-scenario NPV model (Base, Risk, Stress) with Monte Carlo simulation and cumulative probability distributions for both supplier offers

Annual cash flow projections (22-year horizon) dis-aggregated by value source: energy, capacity, RECs, legacy agreement migration, and asset sale proceeds

Tornado/sensitivity analysis identifying primary NPV drivers and quantifying their relative impact under each contract

Stress test analysis determining the market energy price CAGR at which each PPA generates zero net value

Structured qualitative and quantitative comparison matrix across commercial, financial, and risk dimensions

Executive recommendation with supporting rationale across all modeled scenarios

Results & Impact - Base Scenario

Under the Base scenario — assessed as the most likely outcome — Supplier A was estimated to deliver approximately $60M USD in additional NPV versus Supplier B over the analysis horizon, driven primarily by higher energy and REC surplus revenues in the first seven years of the contract when market price certainty was greatest. The stochastic model confirmed this finding across the majority of the probability distribution.

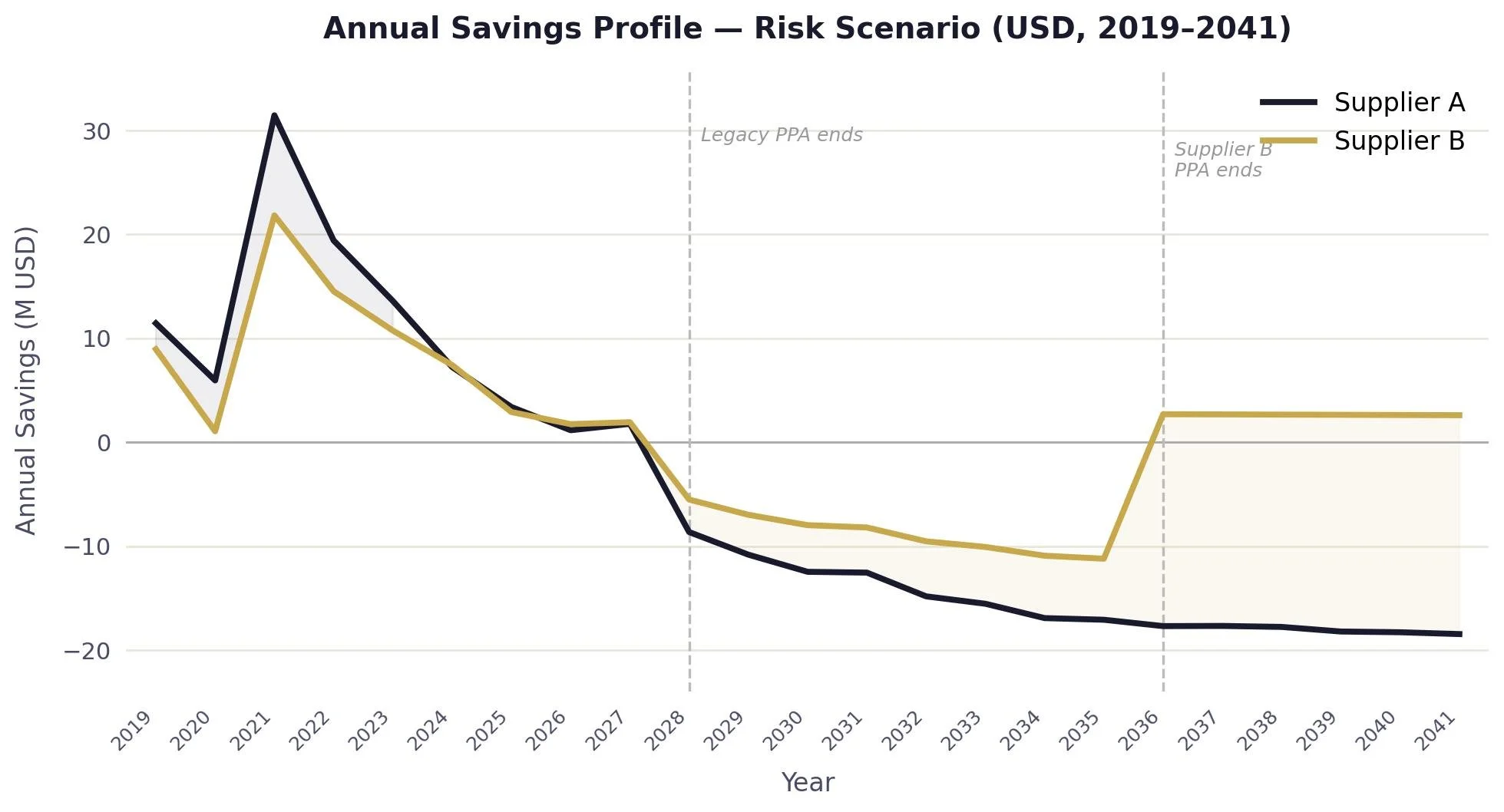

Results & Impact - Risk Scenario

Under the Risk scenario, the NPV advantage of Supplier A narrowed substantially, converging with Supplier B as accelerated market price deterioration and renewable oversupply eroded the value of Supplier A’s larger, longer, as-produced volume position. Stress testing revealed that Supplier A’s NPV reached zero at a market energy price CAGR of −8%, versus −10% for Supplier B — reflecting Supplier B’s greater structural resilience due to its shorter term, fixed volume, and guaranteed delivery profile.

Conclusion

The engagement concluded with a recommendation in favor of Supplier A, grounded in the probability-weighted assessment that the Base scenario was more likely than the Risk scenario, and that the incremental ~$60M USD NPV advantage — concentrated in the near-term years where confidence was highest — outweighed Supplier B’s downside protection benefit.